Canada

Canada

US

US

X

Get started with TD Direct Investing

Guaranteed Investment Certificate (GIC) interest rates in Canada

A Guaranteed Investment Certificate (GIC) is a safe and secure way to help grow your investment. You’ll never lose the money you invest and can choose a GIC that provides a guaranteed rate of return. GICs provide flexible terms and payment schedules and can be held within registered savings plans. There aren’t many guarantees when it comes to investing, except when it comes to GICs. This article will help explain the various types of GICs available and what to look for when picking one that’s right for you.

What is a GIC?

GIC Definition

A GIC is a safe and secure form of investment that lets you grow your money with confidence. You agree to invest a specific amount of money, for a specific length of time. You’ll earn interest on your investment, and once the GIC matures, you’re guaranteed to get 100% of your principal back.

The amount of interest you’ll earn depends on the type of GIC you choose, and the associated interest rate being offered. Interest is earned on a monthly, bi-annual, or annual basis – or whenever the GIC matures.

Typically, the longer you invest, the higher interest rate you’ll earn. GIC terms, or the amount of time you agree to invest, range from 30 days to 10 years.

GIC Rates Calculation

GICs work like savings accounts, paying you interest on your investment. The amount of interest you earn will vary depending on the type of GIC you choose.

GIC rates are determined using either simple interest, or compound interest. With simple interest, you’ll only earn interest on your initial investment. Compound interest is paid on the principal, plus any previous interest earned. With compound interest, you’ll earn a little bit extra on every payment, which can make a big difference over the term of your investment.

Should You Invest in a GIC?

Benefits of Investing in GICs

With GICs, your investment is literally guaranteed. You’ll always get 100% of your initial investment back, and with fixed rates, your returns are guaranteed as well. You have the option to choose how much to invest, and how long to invest it. Payment arrangements can be flexible, letting you pick a payment frequency that works for you.

GIC Investment Downturns

Your investment is typically locked in for the term of the GIC so you won’t be able to access it. GICs also pay low-returns relative to higher risk investments like stocks. If the return rate is too low, you could end up losing value due to inflation and taxes. Income earned on a GIC is taxed at your marginal tax rate.

How to Choose Your GIC Investment?

Types of GICs

There are several types of GICs to choose from, making it easy to find one that works for you.

Cashable GICs: Cashable GICs provide a mix of certainty and flexibility. They are usually limited to a 1-year term and let you withdraw your money after as little as 30 to 90 days. That way, if interest rates go up, you can withdraw your money earlier and invest it in something with a higher return. If interest rates drop, you’re still guaranteed to earn the previously agreed upon rate. Because they’re so flexible, cashable GICs tend to offer lower interest rates.

Non-cashable GICs: If you’re looking for a guaranteed return, consider a non-cashable GIC. Your investment will be locked in for a certain period of time, typically between 30 days to 5 years. The interest rate you earn will be guaranteed for the length of your investment.

Market Growth GICs: Those looking for higher growth potential should consider market growth GICs. These GICs are linked to growth within a specific stock market. The amount of interest you earn will depend on how well that particular stock market performs. Your interest rate isn’t guaranteed, but if the market performs well, your potential earnings can be higher. Your principal investment is still guaranteed.

Registered / Non-registered GICs: Registered GICs are held within Registered Retirement Savings Plans (RRSPs), Tax Free Savings Accounts (TFSAs), or other registered accounts. GICs held within a RRSP grow on a tax deferred basis. Interest earned on GICs held within TFSAs can be withdrawn tax free. Just be sure to comply with any contribution limits attached to the registered account.

Non-registered GICs are held outside of a registered savings plan. You’ll have to pay tax on any interest earned from a non-registered GIC, but there are no limits on how much you can invest.

Redeemable / Non-redeemable GICs: Redeemable GICs let you withdraw your money early, similar to a cashable GIC. Unlike cashable GICs, redeemable GICs aren’t usually subject to 30 to 90-day waiting periods. Non-cashable GICs are locked in for the term of your investment. If you want to withdraw your money early, you’ll have to pay a penalty. Non-redeemable GICs will typically pay a higher interest rate in exchange for you locking in your investment.

Foreign currency GICs: These are GICs held in a foreign currency, such as U.S. dollars.

Escalator GICs: Escalator GICs pay a higher interest rate every year. While you might only earn 2% in year one, you may earn 3% in year two, and so on. This can help counter-act any negative effects of inflation on the value of your investment. Escalator GICs can offer other benefits as well, including the ability to switch your investment to a different GIC every year.

GIC Terms

GIC terms typically range from 30 days to 5 years, although 7 or 10-year terms are also available. That way, you can choose how long to invest. If you’re saving for the long-term, consider a long-term GIC. If you think you’ll need your money back sooner, a short-term GIC may be for you. It's important to choose the term carefully as you will not be able to access the funds before the term ends.

Short-term GICs: Your money is only locked in for less than a year, giving you the option to withdraw it sooner. Short-term GICs typically provide a lower guaranteed interest rate.

Long-term GICs: Your money is locked in for a year or more. Long-term GICs typically provide a higher interest rate and are better suited for long-term savings goals.

GIC Interest Rates

The amount of interest you earn on your GIC, sometimes also called annual percentage yields (APY), will depend on whether you select a fixed, variable, or escalating interest rate.

Fixed interest rates guarantee you’ll earn a specific amount of interest over the term of your investment. With fixed rates, you’ll know exactly how much your investment will earn.

Variable interest rates will rise and fall over the term of your investment. You’ll earn more as interest rates go up, but less if they go down.

Escalating interest rates are fixed and are designed to increase every year. The longer you invest, the higher the interest rate will climb.

Most financial institutions pay out interest annually or when the GIC matures. However other payment frequencies, including monthly or bi-annual payments, may be available.

How to get the most out of GICs?

Think about the long-term

Long-term GICs tend to offer higher interest rates. If you’re saving up for a long-term purchase, such as buying a new home, consider investing in a long-term GIC. Your money will be locked in for a longer period, but you’re more likely to earn a higher rate of return.

Use GICs to mitigate risk within your portfolio

GICs don’t typically pay much interest, but they don’t pose much risk either. Consider using GICs to help balance the risk of stocks or other higher risk investments within your portfolio. If your higher risk investments don’t grow as you hoped, having some GICs in your portfolio can help mitigate any losses.

Consider investing with a financial institution that's a CDIC member

Canadian Deposit Insurance Corporation (CDIC) protects eligible deposits in Canadian and foreign currency for up to $100,000 (Canadian dollars) in each of CDIC's insurance categories. So, if you purchase your GICs from a financial institution that's a CDIC member, your deposits are covered for up to $100,000 per eligible account.

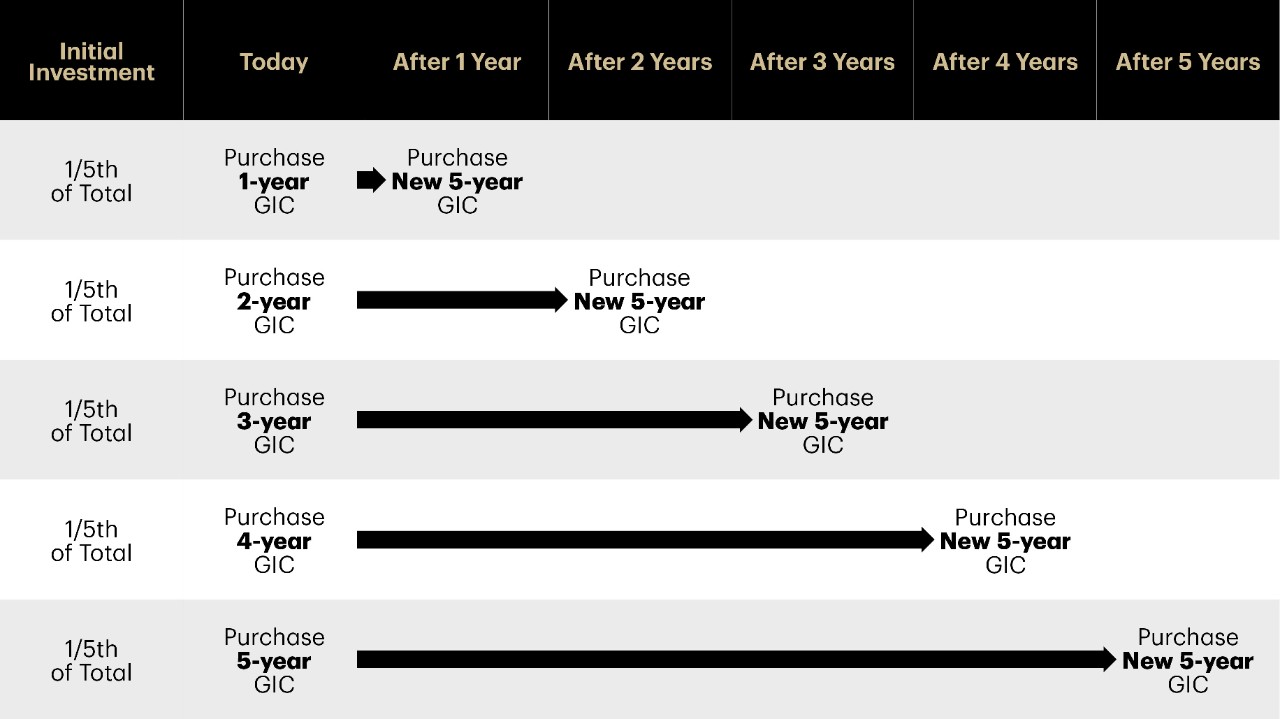

Consider laddering your GICs

Dividing your investment into multiple GICs with different terms is called laddering. Instead of investing everything into one GIC, investors divide their principal into 5 different GICs. Each GIC will have a different term, ranging from 1 to 10 years. That way, one of your GICs will mature every year. You can then take the money you earned and re-invest it in another GIC. Laddering GICs offers more flexibility and will typically result in higher returns over the long-term.

How to buy a GIC

GICs can be bought from a variety of financial institutions, including a brokerage firm, bank, credit union, or trust company.

You can also invest on your own through an online brokerage, like TD Direct Investing. TD Direct Investing uses WebBroker to make buying GICs easy. You can search GICs by rate, term and type and view offerings from various financial institutions. Once you find a GIC that’s right for you, just click and trade.

GIC rates comparison - find top GIC rates with WebBroker

As a TD Direct Investing customer, you can easily review GIC rates offered by various financial institutions and place an order online using WebBroker, a platform from TD Direct Investing. Rates offered as of May 31, 2024 are shown below. For most current GIC rates, please login to WebBroker to access the rate chart.

Short-Term GICs

|

|

30-59 Days |

60-89 Days |

90-119 Days |

120-179 Days |

180-269 Days |

270-364 Days |

|

|---|---|---|---|---|---|---|---|

|

<1 Year |

TD BK US$ |

3.80% |

3.95% |

4.10% |

4.15% |

4.20% |

4.25% |

|

<1 Year |

TD BK US$ |

3.80% |

3.95% |

4.10% |

4.15% |

4.20% |

4.25% |

|

<1 Year |

TD BK US$ |

3.80% |

3.95% |

4.10% |

4.15% |

4.20% |

4.25% |

|

<1 Year |

CDA TR |

3.00% |

3.10% |

4.10% |

4.15% |

4.20% |

4.20% |

|

<1 Year |

TD BK |

3.00% |

3.10% |

4.10% |

4.15% |

4.20% |

4.20% |

|

<1 Year |

TD MTG |

3.00% |

3.10% |

4.10% |

4.15% |

4.20% |

4.20% |

|

<1 Year |

TD PAC MTG |

3.00% |

3.10% |

4.10% |

4.15% |

4.20% |

4.20% |

Long-Term GICs - 1 Year

|

Issuer |

Monthly |

Semi-Annual |

Annual |

Compound Annual |

|

|---|---|---|---|---|---|

|

1 Year |

HOME BANK |

4.99% |

5.04% |

5.09% |

- |

|

1 Year |

EQUITABLE TRUST |

4.97% |

5.02% |

5.06% |

- |

|

1 Year |

LAURENTIAN BANK |

4.69% |

4.81% |

5.06% |

- |

|

1 Year |

CONCENTRA BANK |

- |

- |

5.06% |

- |

|

1 Year |

EQUITABLE BANK |

4.97% |

5.02% |

5.06% |

- |

|

1 Year |

B2B BANK |

4.69% |

4.81% |

5.06% |

- |

|

1 Year |

CANADIAN WESTERN BK |

4.78% |

- |

5.03% |

- |

|

1 Year |

HOMEEQUITY BANK |

4.91% |

4.96% |

5.00% |

- |

|

1 Year |

SCOTIA MORTGAGE CORP |

4.83% |

4.88% |

4.95% |

- |

|

1 Year |

HOMEEQUITY BANK |

4.91% |

4.96% |

5.00% |

- |

|

1 Year |

SCOTIA MORTGAGE CORP |

4.83% |

4.88% |

4.95% |

- |

|

1 Year |

TD MTG |

4.95% |

4.95% |

4.95% |

- |

|

1 Year |

TD PAC MTG |

4.95% |

4.95% |

4.95% |

- |

|

1 Year |

BANK OF NOVA SCOTIA |

4.83% |

4.88% |

4.95% |

- |

|

1 Year |

TD BK |

- |

- |

4.95% |

- |

|

1 Year |

CDA TR |

4.95% |

4.95% |

4.95% |

- |

|

1 Year |

ROYAL BANK OF CANADA |

4.84% |

4.89% |

4.95% |

- |

|

1 Year |

BNS TRUST COMPANY |

4.83% |

4.88% |

4.95% |

- |

|

1 Year |

NATIONAL TR COMPANY |

4.83% |

4.88% |

4.95% |

- |

|

1 Year |

MONTREAL TR CO CDA |

4.83% |

4.88% |

4.95% |

- |

|

1 Year |

BANK OF MONTREAL |

4.75% |

4.80% |

4.90% |

- |

|

1 Year |

CANADIAN TIRE BANK |

4.70% |

4.80% |

4.90% |

- |

|

1 Year |

CANADIAN TIRE BANK |

4.95% |

5.05% |

5.15% |

- |

|

1 Year |

TD MTG US$ |

- |

- |

4.75% |

- |

|

1 Year |

RFA BANK OF CANADA |

4.40% |

4.45% |

4.50% |

- |

|

1 Year |

MANULIFE BK |

4.40% |

4.45% |

4.50% |

- |

|

1 Year |

PC BANK |

3.90% |

3.95% |

4.00% |

- |

|

1 Year |

FAIRSTONE BANK |

3.30% |

3.40% |

3.50% |

- |

Long-Term GICs - 2 Year

|

Issuer |

Monthly |

Semi-Annual |

Annual |

Compound Annual |

|

|---|---|---|---|---|---|

|

2 Year |

HOME BANK |

4.84% |

4.89% |

4.94% |

4.94% |

|

2 Year |

EQUITABLE BANK |

4.84% |

4.89% |

4.93% |

4.93% |

|

2 Year |

EQUITABLE TRUST |

4.84% |

4.89% |

4.93% |

4.93% |

|

2 Year |

CONCENTRA BANK |

- |

- |

4.93% |

4.93% |

|

2 Year |

HOMEEQUITY BANK |

4.83% |

4.88% |

4.92% |

4.92% |

|

2 Year |

B2B BANK |

4.54% |

4.66% |

4.91% |

4.91% |

|

2 Year |

CANADIAN WESTERN BK |

4.66% |

- |

4.91% |

4.91% |

|

2 Year |

LAURENTIAN BANK |

4.54% |

4.66% |

4.91% |

4.91% |

|

2 Year |

MANULIFE BK |

4.60% |

4.65% |

4.70% |

4.70% |

|

2 Year |

MONTREAL TR CO CDA |

4.53% |

4.58% |

4.65% |

4.65% |

|

2 Year |

BANK OF NOVA SCOTIA |

4.53% |

4.58% |

4.65% |

4.65% |

|

2 Year |

BNS TRUST COMPANY |

4.53% |

4.58% |

4.65% |

4.65% |

|

2 Year |

NATIONAL TR COMPANY |

4.53% |

4.58% |

4.65% |

4.65% |

|

2 Year |

BANK OF MONTREAL |

4.50% |

4.55% |

4.65% |

4.65% |

|

2 Year |

ROYAL BANK OF CANADA |

4.55% |

4.60% |

4.65% |

4.65% |

|

2 Year |

SCOTIA MORTGAGE CORP |

4.53% |

4.58% |

4.65% |

4.65% |

|

2 Year |

CANADIAN TIRE BANK |

4.40% |

4.50% |

4.60% |

4.60% |

|

2 Year |

TD PAC MTG |

4.60% |

4.60% |

4.60% |

4.60% |

|

2 Year |

TD BK |

- |

- |

4.60% |

4.60% |

|

2 Year |

CDA TR |

4.60% |

4.60% |

4.60% |

4.60% |

|

2 Year |

TD MTG |

4.60% |

4.60% |

4.60% |

4.60% |

|

2 Year |

TD MTG US$ |

- |

- |

4.55% |

- |

|

2 Year |

PC BANK |

3.90% |

3.95% |

4.00% |

4.00% |

|

2 Year |

RFA BANK OF CANADA |

3.90% |

3.95% |

4.00% |

4.00% |

|

2 Year |

FAIRSTONE BANK |

3.30% |

3.40% |

3.50% |

3.50% |

Long-Term GICs - 3 Year

|

Issuer |

Monthly |

Semi-Annual |

Annual |

Compound Annual |

|

|---|---|---|---|---|---|

|

3 Year |

HOMEEQUITY BANK |

4.64% |

4.69% |

4.73% |

4.73% |

|

3 Year |

HOME BANK |

4.63% |

4.68% |

4.73% |

4.73% |

|

3 Year |

EQUITABLE BANK |

4.63% |

4.68% |

4.72% |

4.72% |

|

3 Year |

CONCENTRA BANK |

- |

- |

4.72% |

4.72% |

|

3 Year |

EQUITABLE TRUST |

4.63% |

4.68% |

4.72% |

4.72% |

|

3 Year |

CANADIAN WESTERN BK |

4.46% |

5.15% |

4.71% |

4.71% |

|

3 Year |

B2B BANK |

4.34% |

4.46% |

4.71% |

4.71% |

|

3 Year |

LAURENTIAN BANK |

4.34% |

4.46% |

4.71% |

4.71% |

|

3 Year |

PC BANK |

4.56% |

4.61% |

4.66% |

4.66% |

|

3 Year |

CANADIAN TIRE BANK |

4.40% |

4.50% |

4.60% |

4.60% |

|

3 Year |

MANULIFE BK |

4.40% |

4.45% |

4.50% |

4.50% |

|

3 Year |

MONTREAL TR CO CDA |

4.28% |

4.33% |

4.40% |

4.40% |

|

3 Year |

TD MTG |

4.40% |

4.40% |

4.40% |

4.40% |

|

3 Year |

SCOTIA MORTGAGE CORP |

4.28% |

4.33% |

4.40% |

4.40% |

|

3 Year |

ROYAL BANK OF CANADA |

4.31% |

4.35% |

4.40% |

4.40% |

|

3 Year |

NATIONAL TR COMPANY |

4.28% |

4.33% |

4.40% |

4.40% |

|

3 Year |

TD BK |

- |

- |

4.40% |

4.40% |

|

3 Year |

BNS TRUST COMPANY |

4.28% |

4.33% |

4.40% |

4.40% |

|

3 Year |

CDA TR |

4.40% |

4.40% |

4.40% |

4.40% |

|

3 Year |

BANK OF MONTREAL |

4.25% |

4.30% |

4.40% |

4.40% |

|

3 Year |

BANK OF NOVA SCOTIA |

4.28% |

4.33% |

4.40% |

4.40% |

|

3 Year |

TD PAC MTG |

4.40% |

4.40% |

4.40% |

4.40% |

|

3 Year |

TD MTG US$ |

- |

- |

4.30% |

- |

|

3 Year |

FAIRSTONE BANK |

3.30% |

3.40% |

3.50% |

3.50% |

|

3 Year |

RFA BANK OF CANADA |

2.90% |

2.95% |

3.00% |

3.00% |

Long-Term GICs - 4 Year

|

Issuer |

Monthly |

Semi-Annual |

Annual |

Compound Annual |

|

|---|---|---|---|---|---|

|

4 Year |

HOMEEQUITY BANK |

4.51% |

4.56% |

4.60% |

4.60% |

|

4 Year |

EQUITABLE BANK |

4.48% |

4.53% |

4.57% |

4.57% |

|

4 Year |

HOME BANK |

4.47% |

4.52% |

4.57% |

4.57% |

|

4 Year |

CONCENTRA BANK |

- |

- |

4.57% |

4.57% |

|

4 Year |

EQUITABLE TRUST |

4.48% |

4.53% |

4.57% |

4.57% |

|

4 Year |

PC BANK |

4.45% |

4.50% |

4.55% |

4.55% |

|

4 Year |

MANULIFE BK |

4.40% |

4.45% |

4.50% |

4.50% |

|

4 Year |

CANADIAN TIRE BANK |

4.28% |

4.38% |

4.48% |

4.48% |

|

4 Year |

CANADIAN WESTERN BK |

4.15% |

- |

4.40% |

4.40% |

|

4 Year |

FAIRSTONE BANK |

4.03% |

4.15% |

4.40% |

4.40% |

|

4 Year |

B2B BANK |

4.03% |

4.15% |

4.40% |

4.40% |

|

4 Year |

MONTREAL TR CO CDA |

4.23% |

4.28% |

4.35% |

4.35% |

|

4 Year |

ROYAL BANK OF CANADA |

4.27% |

4.30% |

4.35% |

4.35% |

|

4 Year |

CDA TR |

4.35% |

4.35% |

4.35% |

4.35% |

|

4 Year |

SCOTIA MORTGAGE CORP |

4.23% |

4.28% |

4.35% |

4.35% |

|

4 Year |

BANK OF MONTREAL |

4.20% |

4.25% |

4.35% |

4.35% |

|

4 Year |

TD BK |

- |

- |

4.35% |

4.35% |

|

4 Year |

TD MTG |

4.35% |

4.35% |

4.35% |

4.35% |

|

4 Year |

BANK OF NOVA SCOTIA |

4.23% |

4.28% |

4.35% |

4.35% |

|

4 Year |

TD PAC MTG |

4.35% |

4.35% |

4.35% |

4.35% |

|

4 Year |

BNS TRUST COMPANY |

4.23% |

4.28% |

4.35% |

4.35% |

|

4 Year |

NATIONAL TR COMPANY |

4.23% |

4.28% |

4.35% |

4.35% |

|

4 Year |

TD MTG US$ |

- |

- |

4.30% |

- |

|

4 Year |

FAIRSTONE BANK |

3.30% |

3.40% |

3.50% |

3.50% |

|

4 Year |

RFA BANK OF CANADA |

2.90% |

2.95% |

3.00% |

3.00% |

Long-Term GICs - 5 Year

|

Issuer |

Monthly |

Semi-Annual |

Annual |

Compound Annual |

|

|---|---|---|---|---|---|

|

5 Year |

HOME BANK |

4.49% |

4.54% |

4.59% |

4.59% |

|

5 Year |

EQUITABLE BANK |

4.48% |

4.53% |

4.57% |

4.57% |

|

5 Year |

HOMEEQUITY BANK |

4.48% |

4.53% |

4.57% |

4.57% |

|

5 Year |

EQUITABLE TRUST |

4.48% |

4.53% |

4.57% |

4.57% |

|

5 Year |

CONCENTRA BANK |

- |

- |

4.57% |

4.57% |

|

5 Year |

CANADIAN WESTERN BK |

4.27% |

- |

4.52% |

4.52% |

|

5 Year |

PC BANK |

4.42% |

4.47% |

4.52% |

4.52% |

|

5 Year |

MANULIFE BK |

4.40% |

4.45% |

4.50% |

4.50% |

|

5 Year |

CANADIAN TIRE BANK |

4.28% |

4.38% |

4.48% |

4.48% |

|

5 Year |

TD MTG US$ |

- |

- |

4.30% |

- |

|

5 Year |

ROYAL BANK OF CANADA |

4.17% |

4.21% |

4.25% |

4.25% |

|

5 Year |

MONTREAL TR CO CDA |

4.13% |

4.18% |

4.25% |

4.25% |

|

5 Year |

NATIONAL TR COMPANY |

4.13% |

4.18% |

4.25% |

4.25% |

|

5 Year |

TD PAC MTG |

4.25% |

4.25% |

4.25% |

4.25% |

|

5 Year |

BANK OF MONTREAL |

4.10% |

4.15% |

4.25% |

4.25% |

|

5 Year |

TD MTG |

4.25% |

4.25% |

4.25% |

4.25% |

|

5 Year |

B2B BANK |

3.88% |

4.00% |

4.25% |

4.25% |

|

5 Year |

BANK OF NOVA SCOTIA |

4.13% |

4.18% |

4.25% |

4.25% |

|

5 Year |

BNS TRUST COMPANY |

4.13% |

4.18% |

4.25% |

4.25% |

|

5 Year |

TD BK |

- |

- |

4.25% |

4.25% |

|

5 Year |

CDA TR |

4.25% |

4.25% |

4.25% |

4.25% |

|

5 Year |

LAURENTIAN BANK |

3.88% |

4.00% |

4.25% |

4.25% |

|

5 Year |

SCOTIA MORTGAGE CORP |

4.13% |

4.18% |

4.25% |

4.25% |

|

5 Year |

FAIRSTONE BANK |

3.30% |

3.40% |

3.50% |

3.50% |

|

5 Year |

RFA BANK OF CANADA |

2.90% |

2.95% |

3.00% |

3.00% |

Cashable GICs

|

Issuer/ Product |

Monthly |

Annual |

At Maturity |

|

|---|---|---|---|---|

|

1 Year |

CDATR 1Y CSHB NONREG |

- |

- |

3.35% |

|

1 Year |

TDBK 1Y CASHBL REG |

- |

- |

3.35% |

|

1 Year |

CDATR 1Y CASHBL REG |

- |

- |

3.35% |

|

1 Year |

TDBK 1Y CSHBL NONREG |

3.35% |

- |

3.35% |

|

1 Year |

TDMTG 1Y US$ NONREG |

- |

- |

3.00% |

|

3 Year |

TDB 3YR PREM CASH |

- |

3.50% |

- |

|

3 Year |

CTC 3YR PREM CASH |

- |

3.50% |

- |

Market-Linked GICs

|

|

|

|

|

|---|---|---|---|

|

3 Year |

TD CDN BANKS 3YR |

S&P/TSX Bank Index |

10.000% - 25.000% |

|

3 Year |

TD US TOP500 3YR |

S&P 500 |

7.500% - 20.000% |

|

3 Year |

TD CD BK&UTL 3YR |

50% S&P/TSX Banks - 50% S&P/TSX Capped Utilies |

6.000% - 30.000% |

|

5 Year |

TD CDN BANKS 5YR |

S&P/TSX Bank Index |

20.000% - 35.000% |

|

5 Year |

TD CD BK&UTL 5YR |

50% S&P/TSX Banks - 50% S&P/TSX Capped Utilies |

15.000% - 50.000% |

|

5 Year |

TD US TOP500 5YR |

S&P 500 |

12.000% - 32.000% |

GIC maturity

When the GIC matures, the principal and interest is credited to your account on the maturity date. It can be seen under the cash balances, which means it’s available as cash that can be withdrawn or reinvested. Please note, GIC auto-renew/rollover is not available for direct investing clients.

FAQs Related to GIC Rates

What are the best GIC rates in Canada?

You can use the GIC rate chart available in WebBroker to compare rates offered by different Canadian banks or financial institutions to find the best GIC rate for you.

Do you pay taxes on GIC investments?

Interest paid on non-registered GICs will be taxed as income in the year it is earned. GICs held within a RRSP will grow tax free until you withdraw your earnings. Interest earned on a GIC held within a TFSA can be withdrawn tax free.

How does inflation affect GIC investments?

GIC interest rates are typically low. If the interest rate you earn is lower than the rate of inflation, you’ll end up losing purchasing power. Investors refer to this as ’capital erosion’. Before selecting a GIC, make sure you know how much interest you need to earn to stay ahead.

Can you lose your money when you invest in GIC?

No. You’re guaranteed to get 100% of your principal back, plus any interest you earn1. A GIC acts just like a savings account. You put your money in, and it earns interest. The only risk is that the interest you earn may end up being less than the rate of inflation. If that’s the case, you won’t end up making much money, but you won’t lose any either.

GICs are a safe and reliable way to help invest. You’re guaranteed to get your original investment back, and with fixed rates, you’ll know exactly how much money you stand to earn. GIC terms are flexible, letting you invest for as little as 30 days, or as long as 10 years. Talk to a TD Financial advisor today about how GICs can help you achieve your financial goals.

Share this article

Related articles

View our learning centre to see how we're ready to help.

Open an account online – it's fast and easy!

Whether you're new to self-directed investing or an experienced trader, we welcome you.